In 2017, almost 10 years after the start of the Global Financial Crisis (GFC), the Basel Committee and the European Systemic Risk Board (ESRB) issued a report that called on the European Commission to introduce a harmonised legislative recovery and resolution framework for insurers and reinsurers. In 2018, the International Association of Insurance Supervisors (IAIS) published the ‘Draft Application Paper on Recovery Planning’ that provided guidance on the key elements of a recovery plan to support financial distress.

Recovery planning is now being incorporated into the Australian Prudential Regulation Authority’s (APRA) supervisory approach for regulated institutions. In order to prepare a credible recovery plan, an insurer will need to do a lot of analysis, workshops, communication, framework alignment and both strategic and tactical thinking. Lets tackle some important questions:

- What are the objectives of the recovery plan?

- What should the recovery plan include?

- Where does it fit into resilience spectrum?

- How will regulators evaluate the quality of the recovery plan?

Regulators have no appetite for failures

Since the collapse of HIH Insurance in 2001, APRA has been one of the world’s most proactive and forward looking financial regulators. APRA’s vision is “to deliver a sound and resilient financial system, founded on excellence in prudential supervision”.

Many have said that APRA’s prudential standards and proactive regulatory approach helped minimise the impact of the GFC on the Australian economy from mid 2007 to early 2009 when, around the world, millions of people lost their jobs as the largest and most sophisticated and advanced economies experienced their deepest recessions since the Great Depression of the 1930s.

To help achieve its vision, each year APRA reveals it’s policy and supervision priorities or key actions. For 2021 and 2022, APRA will continue to develop policies to strengthen an institution’s resilience and preparedness for managing through periods of stress, including recovery and resolution planning, operational resilience, stress testing and climate-related financial risks.

For APRA, the resilience and recovery planning journey started back in 2018/2019. APRA required all health insurers develop a recovery plan. Also on the agenda is the development of a new prudential standard on resolution and recovery planning, taking into account the results of a thematic review with a group of large and medium-sized general insurers and life insurers and lessons learnt from the COVID-19 pandemic.

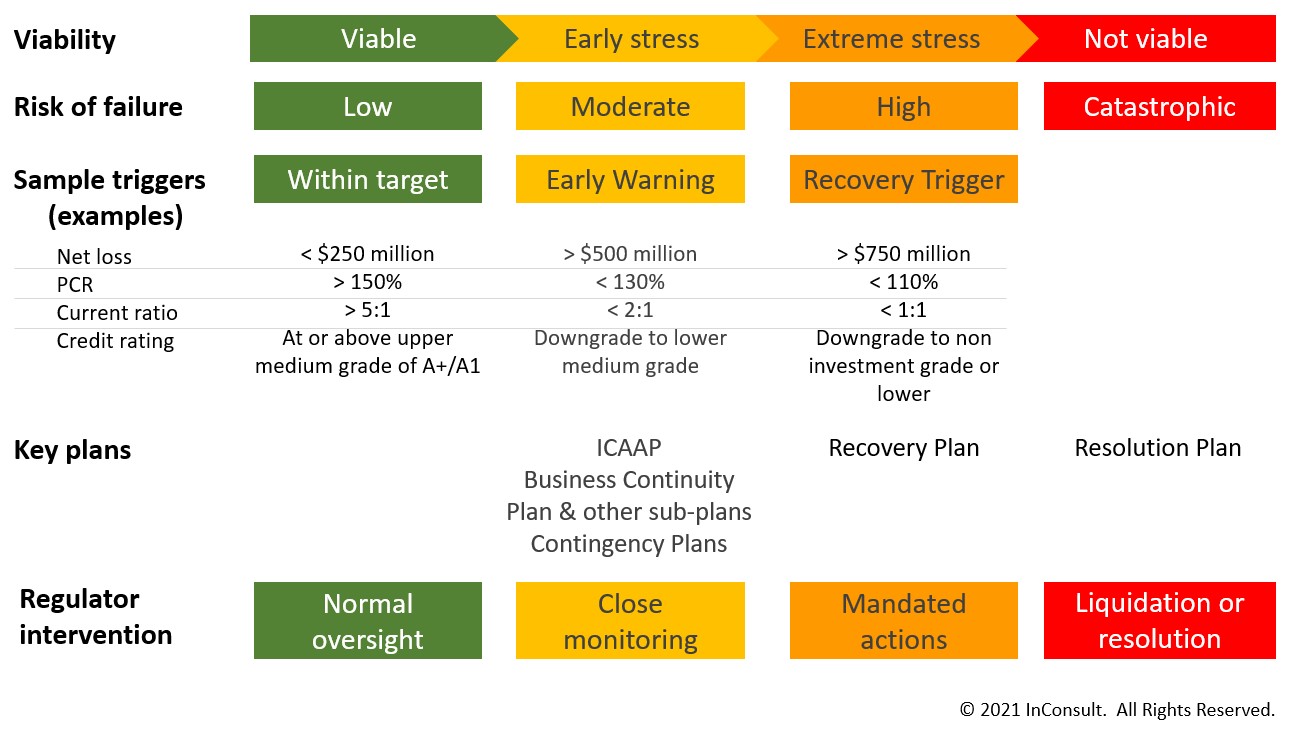

The financial stress continuum

Organisations should understand the relationships between financial viability, early warning indicators, recovery triggers, the respective plans invoked, and the actions taken by the regulator. This relationship is illustrated in figure 1 below as a guide – note the sample triggers are examples only.

Clearly, organisations should operate in the viable stage which is business as usual. In this stage, the risk of failure is low, all triggers are within risk appetite and the normal target range.

As adverse events occur, organisations may move into the early stress stage or extreme stress range where the early triggers and warnings are outside risk appetite or the target operating range. In this environment, a range of plans will come into play including the recovery plan. Regulator monitoring is now more intensive.

Where recovery is not possible, the resolution plan is activated by the regulator. At this point, the insurer is no longer viable and has no reasonable prospect of becoming viable.

What is recovery planning

As defined in the IAIS glossary, a “recovery plan” is a plan that “identifies in advance options to restore the financial position and viability if the insurer comes under severe stress”. A recovery plan should at minimum cover three elements:

- Credible options (menu of actions) to cope with a range of severe stress scenarios.

- Scenarios that address capital shortfall and liquidity pressures.

- Processes to ensure timely implementation of effective recovery options in a range of severe stress situations.

The recovery plan is developed, implemented, maintained, reviewed and tested by the insurer. For the plan to be appropriate and credible, additional analysis and information is required.

Recovery plan content

From our experience, better practice guidelines such as the IAIS Application Paper on Recovery Planning 2019 and APRA guidelines, we suggest the recovery plan cover, at minimum, the following sections:

Executive summary

This is a standalone summary of the material components of the recovery plan, including an overview of governance arrangements, early warning indicators and trigger framework, recovery options and communication strategy.

Background information

A brief overview of the organisation including core business, business model, structure, and interdependencies. This helps to contextualise the recovery plan to the organisation.

The background information section will also help the regulator better understand the organisation to help assess the appropriateness of the trigger framework, scenario tests performed and recovery options included.

Governance

This section should include a description of the monitoring, review and testing activities, plan ownership, related frameworks, and respective roles and responsibilities of key stakeholders (and alternates) during the business-as-usual phase and the recovery phase.

Effective governance arrangements are critical when developing, maintaining and invoking the recovery plan. It outlines responsibilities for monitoring and timely escalation processes for starting the implementation of recovery options.

Plan ownership should be clear, as well as all other responsibilities for key activities.

The recovery plan should be approved by the Board or Senior Officer outside Australia for a branch general insurer.

The recovery plan should be integrated and aligned to other plans and frameworks an organisation has in place e.g. risk management framework, capital management plans, liquidity management, crisis management plan, business continuity plan, etc.

The plan should be be reviewed regularly and updated for material changes to the environment, strategy, structure or activities of the organisation.

Will the plan work when it’s activated? At minimum, it is good practice the plan be operationally tested annually and any opportunities for improvement be incorporated in the recovery plan. The key benefit of testing is to help calibrate triggers, scenarios and recovery options.

Trigger framework

A trigger is an early warning indicator to a potential issue. Triggers are a red flag to a potential issue, but triggers may not result in activation of the plan.

This section should include a sufficient range of relevant early warning indicators and triggers, including both qualitative and quantitative metrics to allow timely escalation, decision-making and invoking the recovery plan.

In line with good practice, the key here is to have a range of metrics and timely trigger points in place to alert management, escalate if required and start the recovery planning process.

The trigger framework should be appropriate to the organisation, and hence the importance of the background information section. The scenario analysis helps to inform the trigger framework.

Some examples of triggers that insurers may consider:

- large insurance losses

- catastrophic losses over the reinsurance limits

- failure or downgrade of a reinsurer

- large investment losses or deterioration in investment values

- deteriorating capital

- reduction in capital ratio’s

- material increase in minimum capital requirements

- material reduction in new business or renewals

- sustained decrease in profitability

- deterioration in liquidity

- credit rating downgrade

- operational event that threatens financial viability or severe financial loss e.g. cyber attack

- adverse judicial interpretations

- external market forces e.g. aggressive competition, new market entrant

- adverse macroeconomic factors e.g. changing interest rate, change in government regulation and fiscal policy

- any sudden change in net assets

Insurers should not rely on just one hard trigger. Rather, a range of triggers that have a knock on effect are considered better practice.

Recovery options

This section would have to be the most important part of the recovery plan. Why? This is where the insurer should outline the range of credible recovery options which aim to enhance its ability to restore itself to financial soundness and meet policyholder expectations.

APRA expects the menu of recovery options to be comprehensive and generate financial benefits to quickly restore the insurer to a sound financial position.

The combination of scenario analysis and regular testing will help ensure that the menu of recovery options are well and truly exhausted i.e. comprehensive.

Some examples of recovery options may include:

- raising non-equity capital

- raising equity capital

- reducing or suspending dividend payments

- reducing or suspending cash repatriation to holding company

- improving liquidity

- buying more reinsurance

- restructuring reinsurance arrangements

- restructuring the investment portfolio

- management actions such as restructure, cost savings initiatives

- exit unprofitable product lines

- partial or full portfolio transfer/sale

- partial or full portfolio run-off

Simply listing the recovery options is not enough. Each option should contain assumptions, implications on strategy, details as to how it will be operationally implemented and the expected financial benefits.

Communication strategy

Ideally, the insurer should include tailored communication strategies which recognise the different communication needs depending on the recovery option(s) being taken. Timely communication helps maintain stakeholder trust and confidence.

The communication strategy should cover both internal communication e.g. board, staff, and external communication e.g. policyholders, agents, brokers, regulators, key third parties.

Insurers should also consider appropriate disclosure obligations under the Corporations Act 2001 and Australian Securities Exchange Listing Rules where applicable.

Scenario analysis

Scenario analysis helps assess the credibility of the recovery plan, and helps to inform and establish the trigger framework and feasibility of the recovery options.

This section of the plan includes a summary of a range of scenarios used, including the estimated financial impacts.

The scenarios should be tailored to the insurer’s business, risk profile, business model, group structure and needs to be adequate to help to activate the recovery plan. In fact, severe but plausible stress scenarios that may ultimately affect the viability of the insurer are preferred.

When choosing scenarios, they should cover appropriately defined events that are most relevant to the insurer, taking into account the insurer’s risk profile, business model, group structure (if applicable) and other relevant factors. Scenarios can include:

- Idiosyncratic stress events, where the negative impact is specific to an insurer or group. For example:

- mass lapse of policies

- failure of material counterparties

- severe losses through a rogue trader or another conduct risk

- a material major cyber-security breach

- Market-wide stress events and/or macroeconomic events affecting the financial system and/or economy. For example:

- a significant loss or stress in financial markets

- a major change to the interest rate environment

- a high-impact catastrophic event, such as a pandemic or climate-related event

- a significant increase in longevity following a medical breakthrough

- a spike in claims following and unfavourable judicial decision

- A combination of idiosyncratic and market-wide stress events

- Both slow-moving and fast-moving adverse events

Appendix

An appendix of relevant information that may be important to the effective execution of the recovery plan. This may include detailed scenarios, key assumptions, sample communication templates that can be tailored once the plan is activated, a table of scheduled activities etc.

What will regulators look for in a recovery plan?

Regulators like APRA will review and challenge insurers and they will provide feedback. Regulators will review a wide range of recovery plans and set some peer benchmarks.

Regulators will regularly undertake resolvability assessments that evaluate the feasibility of recovery and resolution strategies and their credibility in light of the likely impact of the entity’s failure on the financial system and the overall economy. Regulators will typically assess:

- the extent to which critical financial services, and payment, clearing and settlement functions can continue to be performed

- the nature and extent of intra-group exposures and their impact on recovery and resolution if they need to be unwound

- the capacity of the entity to deliver sufficiently detailed accurate and timely information to support recovery

- the robustness of cross-border cooperation and information sharing arrangements

Where insurers fail to achieve the benchmark or meet the guidelines, regulators will ask them to remediate the gaps and resubmit the recovery plan.

In their assessment of the recovery plan, regulators will typically ask the following questions:

- Is the recovery plan clear, comprehensive and complete?

- Is the plan appropriate and relevant considering the insurers risk profile?

- Is the plan well aligned to the risk management and capital management frameworks?

- Is the menu of recovery options sufficient i.e. wide enough range?

- Are recovery options credible?

- Are the recovery assumptions reasonable?

- Are the stress scenarios sufficiently severe?

- Are the early warning indicators and triggers appropriate for invoking the plan?

- Are the triggers aligned to the results of scenario analysis and stress tests?

- Can the recovery options be implemented in a timely manner?

- Are the execution timeframes feasible?

- Are the roles and responsibilities of the Board and Senior Management clearly defined?

- What evidence is there of engagement with the Board and Senior management?

- Does the communication include all key stakeholders?

- Is the recovery plan regularly reviewed and updated?

- Is the recovery plan tested annually?

What is a resolution plan?

This is really the last resort on the resilience spectrum. The resolution plans kicks in when recovery planning fails.

The resolution plan establishes how the regulator would use their powers to achieve an orderly resolution of the failed institution where recovery is not possible and institution has no reasonable prospect of returning to viability. The resolution plan identifies in advance options for resolving all or part(s) of an institution to maximise the likelihood of an orderly resolution.

The development of the resolution plan is led by the regulator (APRA) and/or resolution authority in consultation with the insurer in advance of any circumstances warranting resolution.

How we can help you on your recovery planning journey

We are here to help strengthen organisational resilience. Our recovery planning capabilities include:

- Helping you prepare a recovery plan that is appropriate to your business environment and risk profile based on the APRA guidelines and better practice guidelines.

- Helping you remediate any concerns or gaps identified by the regulator.

- Perform a comprehensive review of your recovery plan to ensure it is in line with the APRA guideline and better practice guidelines.

- Conduct testing of the recovery plan to identify opportunities for improvement.

Be more resilient to financial stress and contact us to discuss your recovery planning needs.