The term greenwashing was seldom used 20 years ago, but today greenwashing continues to be a key concern for regulators, consumers, investors and other stakeholders. The phrase “greenwashing” was first used in an essay written in 1986 by well-known environmentalist Jay Westerveld, who argued that a hotel business had misrepresented their promotion of towel reuse as part of a larger environmental plan.

Today, consumers’ purchasing and investment decisions are frequently made with environmental, sustainability and ethical considerations in mind. For this reason, companies can benefit by distinguishing themselves in their markets by adopting strong environmental, social and governance (“ESG”) actions. They rely on their ESG credentials in marketing and in some cases have regulatory obligations to, or choose to, disclose and report environmental and ethical aspects of their business, eg their greenhouse gas emissions.

Regulators, in particular the Australian Competition and Consumer Commission (ACCC) and Australian Securities and Investments Commission (ASIC) in Australia, are concerned that because of the importance placed on environmental, sustainable and ethical credentials of products and companies by consumers companies may exaggerate these benefits (“greenwashing”).

For this reason, ACCC and ASIC are prioritising their focus on companies making environmental and other ESG claims about their products or their operations.

What is Greenwashing?

Greenwashing describes misleading conduct that relates to an environmental, sustainable and/or ethical quality of a product, such as over representing the extent to which products or company operations support or do not damage the environment, are sustainable or produced ethically. An intention to mislead is irrelevant.

Greenwashing erodes trust. Misleading conduct can be in representations made in a number of ways including on or in:

- product information

- statements

- company reports

- product names

- company or business names

- labels

- packaging

- advertising and promotional material

- disclosures

- communications

Misleading representations can be:

- words

- pictures

- silence

Companies, however, are not facing new regulations when it comes to prohibitions on greenwashing. Companies and their directors should be familiar with:

The Australian Consumer Law:

- (s18) prohibits conduct that is misleading or deceptive as well as conduct that may mislead or deceive consumers,

- (s29) prohibits the making of specific false and misleading representations including that goods or services have a particular quality, history, performance characteristic or benefit.

The Corporations Act (s1041E, 1041G, 1041H) and the Australian Securities and Investments Commission Act ( s12DA, 12DB):

- prohibit making false or misleading statements and engaging in dishonest, misleading or deceptive conduct in relation to financial products or services.

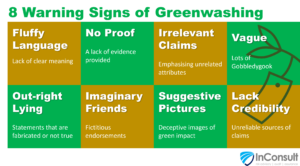

Examples of Greenwashing

So what does greenwashing look like? Here are some examples of greenwashing that range from outright lies to creative ways to tell lies.

- Volkswagen admitted to cheating emissions tests by fitting various vehicles with a “defect” device, with software that could detect when it was undergoing an emissions test and altering the performance to reduce the emissions level

- Before IKEA was connected to illegal logging in Ukraine in June 2020, the furniture company was regarded as a shining example of a large firm being sustainable.

- According to a report released in 2021 by the Rainforest Action Network, major banks such as JP Morgan, Citibank and Bank of America, Wells Fargo, Barclays, Bank of China, HSBC, Goldman Sachs, and Deutsche Bank are still lending massive sums to industries that contribute the most to global warming, such as fossil fuels and deforestation, despite boasting that they are the leaders of the green transition.

- Windex, the glass cleaner by SC Johnson claimed its bottles were made from 100% “ocean plastic”. But in fact, the plastic used to make the bottles was never in the ocean. It was pulled from plastic banks in Indonesia, the Philippines, and Haiti. This type of plastic is known as ocean-bound plastic because it would have otherwise ended up in the ocean.

- Ryanair boldly proclaimed to the British people in early 2020 that it was Europe’s “lowest emissions airline.” The allegation was made up, and the commercials were swiftly prohibited by the Advertising Standards Agency.

- On its website, an issuer makes it clear that it is dedicated to achieving nett zero carbon emissions across all of its investment holdings. However, investors aren’t given any details on how or when it plans to reach this goal.

What Actions are the Regulators Taking to Stop Greenwashing?

The ACCC’s enforcement and compliance policies for 2022-2023 include prioritising the pursuit of businesses that make misleading statements about the environmental and/or sustainable qualities of their goods or services and businesses making misleading claims about the carbon neutrality of their production processes.

ASIC is part of the International Organisation of Securities Commissions Sustainable Finance Task Force which is looking more closely at greenwashing of financial products, including developing a consistent taxonomy to define climate friendly and sustainable financial products and activities.

ASIC is reviewing the practices of managed and superannuation funds making claims that the investment products they offer are as ESG focussed as they claim them to be.

Also, ASIC may be more lenient on companies breaching the Corporations Law and ASIC Act than the ACCC when it comes to financial institutions and any over-representations by them of their environmental, sustainable and ethical practices and investments, focusing, at least initially, on education rather than compliance enforcement.

ASIC conducted a similar review of climate risk disclosures of large, listed companies which showed that the standard of climate-related disclosures has improved over the past few years, however they found that many companies’ disclosures appeared to have a marketing focus, which rings alarm bells.

What Should Businesses do to Reduce the Risk?

Any company, or business with good governance and compliance processes in place should not be too concerned about greenwashing risk.

Companies should make sure that their reports, promotional materials, product statements, labels and representations made in other materials do not create a false or misleading impression for consumers. This is assessed by considering all the circumstances around the representation, such as the nature of the product or services, the consumers’ purchasing decision-making process consumers, the audience, how and where the representation is made.

True/accurate

Representations must be accurate and capable of being substantiated. They need to be made on reasonable grounds, be scientifically sound, and/or evidence based. Claims should not overstate the level of acceptance in the relevant scientific community. Provide easy access to relevant information for consumers.

Concise/clear/unambiguous

Representations must be easy for consumers to understand. They should be free from jargon and vague or confusing terminology that can be misinterpreted. This requires a consideration of the audience and the breadth of knowledge and education they may have. Be specific and clear what aspect of the products, services, packaging or operations a representation relates to.

Specific

Claims should be specific, not general, unqualified statements. Clarify any terminology that doesn’t have a certain or well understood meaning. Information must be consistent across all media and materials.

Disclaimers or qualifications

All caveats, disclaimers or qualifications must be prominent and relate to the original claim but should not be relied on to correct a misleading headline claim.

Real benefit

Only make a claim when there is a genuine benefit or advantage. Do not overstate the benefit. Explain the significance of the benefit claimed.

Predictions of future events need to be based on reasonable grounds. How you can make the statement and achieve the targets/ benefits claimed. This is particularly relevant to company reports and statements including net zero goals. There needs to be an actual plan to get to the represented goals.

Investment strategies

Claims made in respect to investment products should disclose the policy, considerations and methodology adopted to achieve the stated environmental or sustainability outcomes or investment decisions. Explain investment screening processes and criteria.

Targets

Targets should be based on reasonable grounds and describe how and when the target will be met, how progress is measured, and any assumptions relied on in setting the target.

Metrics

Where environmental or sustainability metrics are used, their sources, the underlying data and calculation methodologies and limitations need to be specified.

6 Things to Avoid Greenwashing

Once a company identifies the need to address climate risk, overcoming the internal obstacles should be the focus of those driving climate risk change in the company. The following 6 steps will start you off and overcome these obstacles.

- Include Australian Consumer Law (ACL) and ASIC compliance training for relevant staff.

- Develop a marketing and reporting checklist and sign off procedure.

- Appoint a person responsible for overseeing ACL and ASIC compliance.

- Keep up to date with regulatory developments around disclosures as these are being updated internationally eg the proposed IFRS disclosures standard ( which follows the TCFD framework).

- Understand what standards to use when assessing product or services or the company operations as environmentally or socially responsible.

- Make disclosures in accordance with the reporting framework set out in the Recommendations of the Taskforce on Climate-related Financial Risks (TCFD) for disclosing climate related financial risks and the Taskforce on Nature-related Financial Disclosures (TFND) for disclosing nature related risks of the company.

We Help You Reduce the Risks

Regulators are now holding organisations accountable for misleading ESG claims. Therefore, organisations making ESG related disclosures need to implement periodic process-reviews of ESG related processes.

Some of these reviews can be performed by your organisation’s internal audit, risk management or compliance functions, but the reviews will also require specialist expertise (subject matter experts) in environmental and social sciences for more robust fact-checking and reviews of methodologies. This is where we can help. We can:

- Deliver tailored ESG training to help upskill the Board, management, staff and supply chain.

- Review the robustness of your ESG framework, methodologies and templates.

- Assess your ESG compliance to regulatory requirements.

- Review ESG monitoring metrics and adequacy of reports to stakeholders.

Take steps to reduce the risk of greenwashing and contact us to discuss your needs.