In part 1 of our special 3-part series, we explored the evolving landscape of climate disclosure and sustainability reporting including Australia’s climate change journey, the imminent changes to climate change disclosure and how more than ever, directors will be in the spotlight.

In part 2, we now take a detailed look into the new mandatory sustainability reporting laws as these new laws mean new risks and challenges.

The law

Following a period of consultation, which resulted in some amendments to the proposed climate reporting requirements, on 27 March 2024 the Treasurer introduced the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024 (“Bill”) into Parliament.

Schedule 4 of the Bill proposes a new mandatory climate risk reporting framework for large Australian companies. The Schedule will amend the Corporations Act to include an obligation for certain companies to prepare annual sustainability reports.

The aim of the new legislation is to provide better comparability in data reported by large Australian companies to enable investors to make the right investment decisions to benefit from investment in a net zero transformation and to manage climate change challenges.

The Standards

To accompany the new legislation accounting standards are being developed by the Australian Accounting Standards Board (“AASB”) which will describe in more detail the required content of the disclosures. These are being guided by the International Sustainability Standards Board’s IFRS S1 and IFRS S2 Sustainability Standards to ensure global consistency in reporting, but with some differences to better suit the Australian corporate and reporting environment. Draft ES SR1 Australian Sustainability Reporting Standards-Disclosure of Climate-related Financial Information contains three draft Australian Sustainability Reporting Standards (“ASRS”) (“the Sustainability Standards) and is currently available for review.

One big difference between the proposed ASRS 1 and IFRS S1 is that the Australian Sustainability Standard only refers to climate change disclosures, whereas IFRS S1 encompasses sustainability disclosures more broadly.

To align with the Australian Government’s direction to address climate-related financial disclosures first, the AASB is developing climate-related financial disclosure requirements that can, at least initially, be applied independently of any broader sustainability reporting framework. This approach would permit additional time to consider the development of reporting requirements for other sustainability-related matters in Australia over time.

What will need to be reported?

The Bill along with the draft Sustainability Standards give us guidance on what the basic contents of the annual sustainability report will likely need to include. These are:

- a climate statement in relation to the reporting company for the financial year, including any notes specified by the Sustainability Standards. Required notes will likely include notes on the preparation of climate statements, the statement contents, or other matters concerning environmental sustainability;

- any statements or other specific inclusions prescribed by regulations relating to the statements including those relating to financial matters concerning environmental sustainability; and

- a directors’ declaration that the substantive provisions in the report comply with the Corporations Act and the Sustainability Standards. The Bill proposes a 3-year transition period, where directors need only declare that the company has taken reasonable steps to ensure that the substantive provisions of the report comply.

If a reporting company determines that it has no material climate related risks or opportunities, it will need to disclose that fact in its general-purpose financial reports and explain how it reached this determination.

Climate-related Disclosures

The disclosures must fairly present the entity’s risks and opportunities. The climate statements and notes, when read together, must disclose:

- any material climate-related financial risks and opportunities that could reasonably be expected to affect an entity’s prospects;

- the climate metrics and targets proscribed by the Standards for disclosure including scope 1, scope2 and scope 3 emissions;

- information about governance, strategy, risk management in relation to the risks, opportunities, metrics and targets.

The core content of climate-related financial disclosures will need to contain information from the 4 pillars identified in the TCFD Framework, being governance, strategy, risk management, and metrics and targets.

Audit requirements

The annual sustainability reports will need to be audited in accordance with new assurance standards being developed by The Australian Auditing and Assurance Standards Board (AUASB) and to be phased in from 1 January 2025.

Who will need to report?

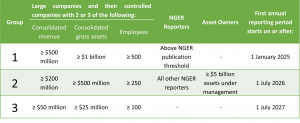

Three classes of entities will be required under the new legislation to prepare sustainability reports:

- Large companies that are required to prepare and lodge annual reports under Chapter 2M of the Corporations Act

- Asset owners (e.g. superannuation companies and registered schemes) with more than $5 billion funds under management

- Any size entity subject to both the annual reporting requirements under the Corporations Act and emissions reporting obligations under the National Greenhouse and Energy Reporting Act 2007.

Although small and medium businesses, below the relevant size thresholds, charities and not-for-profits will be exempt under Bill from reporting, some of these may, be asked by reporting entities in their value chain to disclose similar information to assist the reporting entity to prepare meaningful and accurate disclosures, particularly, in respect to their scope 3 emissions reporting.

When do the reporting obligations begin?

The reporting entities will be classified into 1 of 3 groups with a phased starting period as shown in the table below:

Overcoming the challenges

Other than the compliance challenges that will come from meeting reporting obligations in respect to the entity’s governance, strategy, metrics and targets and risk management, entities will need to consider and overcome some other less obvious challenges.

In part 3, we will delve deeper into some of the challenges and look at strategies to overcome them.

The bottom line

The impending mandatory sustainability reporting requirements mark a pivotal shift in how Australian corporations must address their environmental responsibilities. As the global community intensifies its focus on combating climate change, pollution, and biodiversity loss, Australian companies must prepare for the stringent climate disclosure mandates being legislated.

The path to compliance may be challenging, but the rewards of safeguarding both the planet and long-term business viability are immense.

We are here to help you manage climate risk

By acting now, you can turn these challenges into opportunities, positioning your company as a leader in sustainability and corporate responsibility. Don’t wait for the legislation to take effect—begin your journey towards a more sustainable and resilient future today.

Together, let’s build a more sustainable tomorrow.

Contact us to embark on a journey towards authentic environmental stewardship and responsible business practices.